In the evolving healthcare landscape, concierge medicine has become a popular model for those seeking more personalized care. With this model, patients pay an annual or monthly membership fee, called a retainer fee, for enhanced access to their healthcare providers.

A common question that arises is whether concierge medicine membership fees are tax deductible. This blog post explores the intricacies of tax deductions related to concierge medicine based on current IRS guidelines and interpretations.

Before we dive into the tax implications, it's essential to understand concierge medicine, also known as retainer-based medicine. In this model, patients pay a membership fee for services that typically include:

The goal of concierge medicine is to offer a more personalized healthcare experience, where the doctor can devote more time to each patient compared to traditional healthcare systems.

If concierge medicine membership fees are deductible, the answer is nuanced and depends on the type of services provided. The deductibility of concierge medicine fees depends on whether the payment is for actual medical care received versus solely for access or availability.

A payment that covers actual medical services, such as routine physicals, examinations, and other healthcare services rendered during the tax year, may be deductible if it is paid for them and properly allocated. In contrast, if the fee is merely for doctor access or availability (considered non-medical services), it generally does not qualify for a tax deduction.

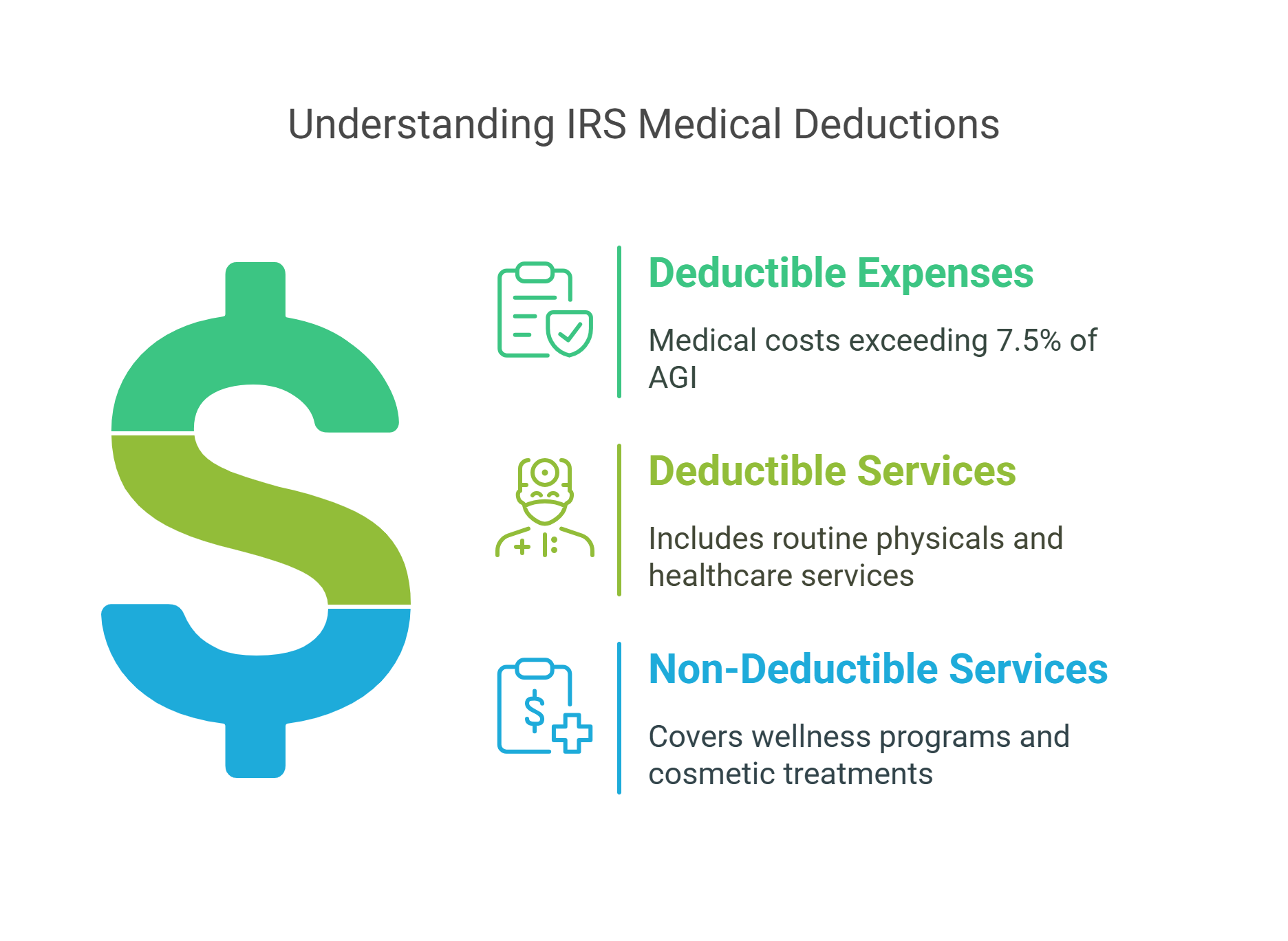

Medical expenses are generally deductible only if you itemize deductions and they exceed 7.5% of your adjusted gross income (AGI). However, not all medical expenses are deductible. According to the Internal Revenue Service (IRS), only the portion of qualified medical expenses that exceed 7.5% of your AGI are potentially deductible.

The IRS defines deductible medical expenses as those paid for the "diagnosis, cure, mitigation, treatment, or prevention of disease," or for treatments affecting the structure or function of the body. Expenses must be primarily to alleviate or prevent a specific physical or mental illness; costs merely beneficial to general health usually don't qualify.

For example, the cost allocated to an annual physical exam or preventative care received during the year as part of the membership may be deductible, while fees purely for access to after-hours communication with the doctor or the ability to get same-day appointments generally are not.

A taxpayer can deduct unreimbursed qualified medical expenses that exceed 7.5% of their adjusted gross income (AGI) when itemizing deductions for the tax year (e.g., 2024 rules apply for returns filed in 2025). Some specific medical service costs potentially covered by concierge membership fees may qualify if properly allocated and documented, but not the entire fee if it includes non-medical access or future services.

To determine if any portion of concierge medicine fees are deductible, it's important to consider the breakdown of services included in the membership:

Medical Services: If portions of the fees are clearly allocated by the provider to specific health-related services rendered during the tax year, such as diagnostic exams, preventive care, or chronic disease management, they may be considered deductible medical expenses.

Non-Medical Services: Fees that are solely for access to a physician, availability, or services that are not directly related to medical care, such as personal wellness consultations or convenience perks, typically do not qualify for tax deductions.

For example, if your concierge practice provides an annual physical and chronic disease management and itemizes the cost for these specific services received during the year, you could potentially deduct the allocated cost related to these medical services, subject to the AGI threshold.

For example, if your AGI is $100,000, your medical expense deduction threshold is $7,500 (7.5% of $100,000). So, if you pay $10,000 in total qualified and unreimbursed medical expenses (which might include an allocated portion of your concierge fee for services rendered, plus other medical costs), you may be able to deduct $2,500 ($10,000 - $7,500). You cannot deduct the portion of the fee that is just for access or availability.

Proper documentation is crucial for those considering deducting any portion of their concierge medicine membership fee. Patients should request a detailed itemized breakdown of services covered by the fee from their healthcare provider, clearly distinguishing charges for medical care received from any fees for access or future services.

This documentation supports the amounts claimed on Schedule A of the tax return to determine which portion of the fee can be potentially deductible. Before claiming a deduction, subtract any reimbursements from insurance and calculate the amount exceeding 7.5% of your AGI from your total qualified medical expenses. Also, be aware of the prepayment rule: generally, you cannot deduct payments made in the current year for medical care that will be provided substantially beyond the end of that year.

Tax laws are complex, and the IRS has not issued specific binding guidance on concierge fees. There are many nuances to what constitutes a deductible medical expense, so it's a good idea to consult a qualified tax professional. A competent accountant can help you evaluate your specific situation, review documentation, and provide personalized advice based on current interpretations of tax law.

Portions of concierge medicine membership fees may be deducted from tax only if they are clearly allocated to specific, qualified medical services rendered during the tax year, and only if the taxpayer itemizes deductions and meets the 7.5% AGI threshold. Fees purely for access or availability are generally not deductible. To determine whether any part of concierge medicine fees are tax deductible, it is important to understand exactly what they cover and ensure appropriate, itemized documentation from the provider. It is imperative to stay informed and seek professional advice to successfully navigate the tax deductibility of concierge medicine fees as interpretations and tax laws can evolve.

Previous Post